I am using the Fidelity 2% CB unlimited card. My monthly spend is pretty high and averages about $8-10K per month with periodic $15K months. My annual rewards are typically about $2,500 per year. A coworker was telling me about his robinhood card that gets him 3%. That extra percent means I am leaving about $100/ month on the table.

I have the Costco Citi Visa, for what I do it’s decent and I get around $600 back on top of my 2% from the Costco Executive membership which more than pays for itself.

I had never heard of that card before now. But, from what I see, that cost is $50 per year There is also a wait list to get the card, with no comment about how long it could take to actually get off of the wait list and receive one. https://www.nerdwallet.com/credit-cards/learn/robinhood-credit-card

I use the approach that former CHB poster Fuzzbutt used - multiple credit cards to maximize rewards. I use the Fidelity Visa 2% card as the catch-all for those purchases that don’t fall under other categories. Some other cards I use, with the relevant percentages that I focus on:

-Pentagon Federal Visa - 5% on gasoline purchases

-Costco Visa - 3% on travel and dining

-Chase Freedom Flex - 3% on dining and drug store purchases, plus 5% quarterly rotating rewards categories

-US Bank Cash+ Visa - 5% on categories we can select, which I use for utilities, internet and fitness club memberships

-Venmo Visa - 3% on the highest spend category per billing cycle. I use this exclusively for supermarkets. The Venmo Visa also categorizes warehouse clubs such as Sam’s Club and Costco as supermarkets, so 3% on those purchases.

-Amazon Visa - 5% on Amazon.com purchases as Prime member

-Target Mastercard - 5% discount on all Target purchases.

That’s probably the best way to squeeze all the value out of credit cards, but I’m too lazy. My kid has a low annual fee travel card that works for him because of work travel and the Marriot and United rewards programs.

The other day Clark was talking about his various credit cards and one of them, an Amex, had a $75 credit at Lululemon every quarter that his wife and daughter uses. I thought that is an odd reward.

I agree. I use a minimalist wallet that carries 2 credit cards, my debit card (that I haven’t used in years), insurance card and cash. I can scan the credit card chip without removing it from the wallet.

From what I experienced, many of these premium rewards have fairly low caps. For example many gas cards have a cap of $200 in rewards… Plus the penalty for accidently forgetting to pay a card will erode all the savings. I am with other and I am too lazy to keep track of several cards.

I agree, but I have 4 cards, one each of the majors - Discover, Citi Mastercard, Costco Visa and Amex Blue Cash. The Citi MC and Discover rebate 1% but have some things each quarter at 5%. Like bears, we are executive members and always get a sufficient rebate on that to pay more than the membership fee. Amex Blue Cash Everyday (no annual fee) has different levels, like the Costco Visa, for different uses. Most useful to us is 3% on groceries, but they also have a lot of one time credits and special rates if you like the things they provide for (which we usually use 2-3x each year). Amex offers a Blue Cash Preferred which doubles all the rebates on the Everyday, but costs $95/year.

Interesting. I just checked that one out and just on groceries I can get $360 back a year, plus they have a $250 bonus when you charge $3,000 in the first six months. Also the first year is no fee, then $95 a year like you said. At least $600 in free money for the first year sounds tempting. The rest of the categories wouldn’t add up to much for me or I’m better off with the Costco card

One of my cycling friends just got back from a trip to Egypt . I don’t know how his wife does it but she plays the travel points game like nobody I’ve ever seen. I retired in 2019 and in that time he and his wife have done these

New Zealand

Antarctica

African (photo) safari

Sweden and Finland

Tahiti

Singapore

Alaska cruise

I have the Blue Cash Everyday card from American Express. When I got it about 4 or 5 years ago, there was a 3 to 4 hundred dollar bonus. There is no annual fee, for is only good for 5 to 6 thousand dollars in purchases a year.

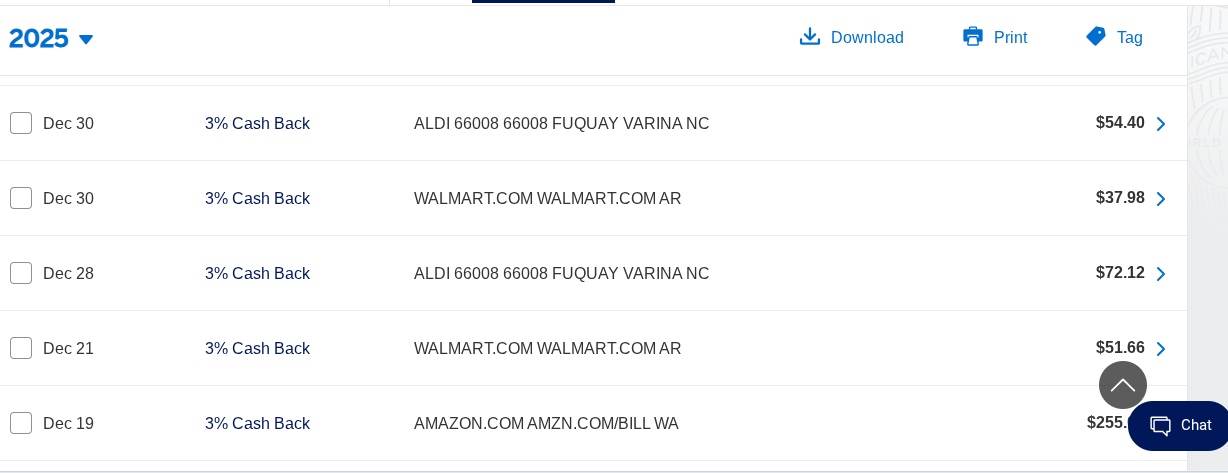

I get 3% back on Purchases from places like Amazon, Aldi’s, Walmart.com and the regular Supermarkets.

Here is an example of some of the purchases that I made in 2025.

100%. Retailers are charged a couple % on every transaction. The thing is that most don’t offer a cash discount because they have to pay a similar fee to the money trucks that pickup and drop-off cash. Tiny local business might offer a cash discount and I will almost always take advantage of that. Since you are going to pay the same price if you use cash, check, debit, or credit, you might as well take the one with the best benefits.